For fifteen years, SaaS pricing has been roughly the same thing: a free tier or trial, three flat-rate plans, an enterprise "talk to sales" tier, and a billing engine that quietly assumed your marginal cost per user was approximately zero. That math worked because Heroku gave you a server for ten bucks and Salesforce ran your CRM on infrastructure you paid for in flat monthly increments. AI broke that math in eighteen months. The companies still pricing like it's 2020 are quietly bleeding margin on every active user — and most of them don't know it yet.

This post is the strategic frame: how software pricing got here, why the AI cost structure is forcing a redesign, and what's actually emerging as the new model. If you're a SaaS founder, this is the conversation to have with your team this quarter — not "should we add an AI feature" but "what does our pricing page look like once those AI features exist." For the tactical follow-up on how to actually layer usage-based pricing on top of subscriptions, see our companion post on usage-based pricing for SaaS.

Software 1.0, 2.0, and 3.0 — the framework that explains why pricing keeps breaking

Pricing models in software aren't arbitrary. They reflect the underlying cost structure of how the software is produced and delivered. When the cost structure changes, pricing changes. We've now been through this three times.

Software 1.0 — perpetual licenses (1980s–2000s). Software ran on the user's computer. The vendor built it once and shipped it on a disk or download. Marginal cost per copy was essentially zero, but the unit of value was a discrete version: Word 95, Word 97, Word 2000. Pricing followed the unit: pay once per license per machine, upgrade when a new version ships. Adobe, Microsoft, QuickBooks, Salesforce in its early days — all priced this way because the underlying delivery model was "an artifact you owned."

Software 2.0 — SaaS subscriptions (2000s–early 2020s). The cloud changed everything. Software no longer lived on the user's computer; it lived on a server somewhere, accessed through a browser. The vendor shipped updates continuously, sometimes hourly. The concept of "version" dissolved. The cost structure shifted: vendors now paid for the servers, the bandwidth, the storage. Critically, those costs scaled cheaply with users — Heroku and AWS made the marginal cost of one more active user effectively trivial.

The pricing model that fit this cost structure was the subscription: pay monthly or yearly for access. Per-seat pricing tracked roughly with usage (more seats = more concurrent users = more compute). Freemium worked because the marginal cost of a free user was near zero — the vendor could absorb thousands of them on the chance that a few percent would convert. This is the era we're all still operating in.

Software 3.0 — subscription plus usage (2024–). AI broke the cost structure. Suddenly the marginal cost per user isn't trivial — it's dollars per generation, depending on the model, prompt length, output length, and how aggressive the user is. A Notion AI user who generates fifty pages of content costs Notion real money. A Canva AI user who generates a hundred images costs Canva real money. The vendor isn't just paying for servers anymore; they're paying retail prices to OpenAI, Anthropic, and Google for every active user's compute.

This isn't a small adjustment. It's a fundamental change in how software cost works. And it requires a new pricing model.

The mistake most SaaS founders are making right now is bolting AI features onto a 2.0 pricing page — same flat tiers, same freemium, same "unlimited usage" promise — without re-pricing for the new cost structure. The result is a business that looks like it's growing while quietly burning margin on every active user. The fix isn't dramatic; it's structural. Software 3.0 pricing is both a subscription layer (for access to the software) and a usage layer (for the compute the AI consumes). Most teams need both.

Why freemium is the first thing that breaks

Freemium was one of the great innovations of the SaaS 2.0 era. The math worked: marginal cost per free user was near-zero, so a vendor could give away unlimited access to a stripped-down version and let conversion economics work in their favor. Slack, Dropbox, Notion, Calendly, hundreds of others — freemium was the standard go-to-market for product-led companies.

Under the AI cost structure, that math collapses. Imagine a stripped-down free Canva that includes a few AI image generations. Each generation costs Canva 50 cents to a dollar in OpenAI fees. A free user who generates a hundred images costs Canva $50-$100 on the way to never converting. Multiply by ten thousand free users a month and the freemium tier is now a six-figure monthly liability.

The teams handling this well are doing one of three things:

Capping AI usage on free tiers. Free users get the non-AI surface unrestricted, but AI generations are limited to N per month. This keeps the cost predictable. The trade-off is that the free tier no longer demonstrates the AI's full power, which is the exact thing that drives upgrades — so conversion rates can drop unless the cap is generous enough to let users feel the value.

Moving AI to a paid-only tier. No AI on free at all; you have to pay to get any AI capability. This is cleaner financially but worse for product-led growth — users can't experience the AI before paying, which raises the bar for trial-to-paid conversion meaningfully.

Replacing freemium with a time-limited free trial. Reverting to the older "30 days of full access, then pay" model. This caps the free-tier cost by capping the duration, not the usage volume. Works well for products where users can form a habit in the trial window; works poorly for products where the value compounds over months.

There's no clean answer here. The teams that are doing this best are running quiet experiments — A/B testing different cap structures, watching their AI-cost-per-free-user metric weekly, and adjusting. The teams that are getting hurt are still operating on "unlimited free AI" promises from a year ago that they haven't yet revisited.

The deeper point: freemium worked because the marginal cost was zero. If your marginal cost isn't zero anymore, freemium needs a redesign. There's no SaaS pricing law that mandates a free tier. There's only the unit economics of your specific cost structure.

The new model: subscription plus usage

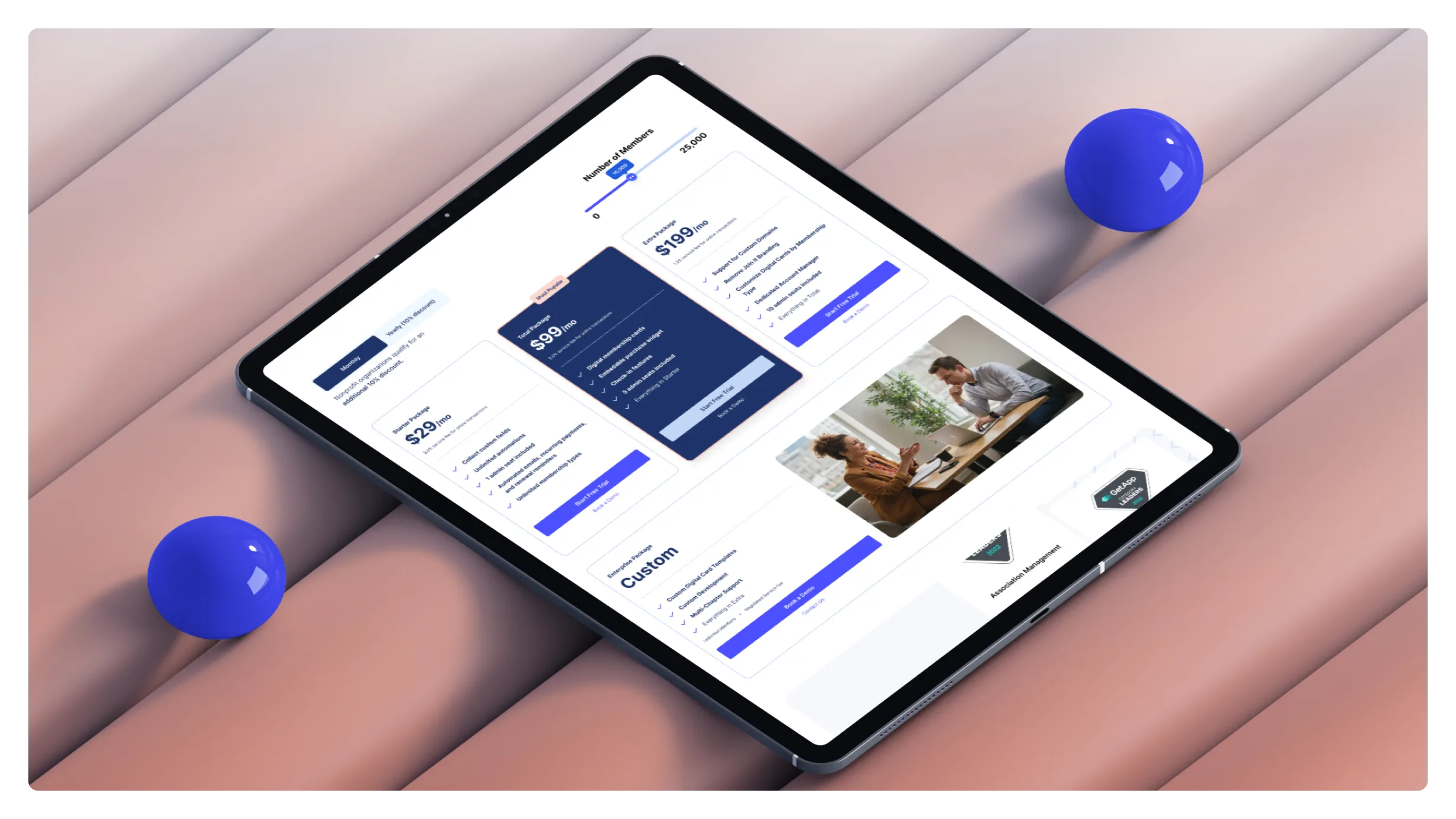

The model that's emerging — and that we think will be the default within eighteen months — is a two-layer pricing page. One layer is the subscription: access to the software, the feature set, the user seats. The other layer is usage: how much AI compute the user consumes. Both layers are visible. Both layers are paid for.

The subscription layer looks like classic SaaS pricing: tiered plans (Starter, Pro, Enterprise), per-seat or per-workspace, monthly or annual. This covers the software's non-AI value — the workflows, integrations, collaboration features, anything that doesn't directly scale with AI compute.

The usage layer sits on top and tracks AI consumption. The two most common patterns:

- Credits — the customer buys a bucket of credits ($10 = 100 credits = X AI actions). The credit-to-action ratio is opaque to the customer but lets the vendor adjust mapping behind the scenes (e.g., image generation = 5 credits, text generation = 1 credit, video generation = 50 credits). This is how OpenAI, Anthropic, Notion, and most early AI-first SaaS products are handling it.

- Token / API-call billing — direct billing per unit of compute. Cleaner technically; worse for non-technical users who don't intuitively understand what a token is.

The reason this two-layer structure is winning is that it cleanly separates two different things: the subscription covers the predictable monthly value of access to the software; the usage covers the unpredictable variable cost of AI compute. The customer can budget the subscription. The vendor can match the usage charge to actual cost. Both sides get what they need.

Cursor is the cleanest example. They charge $20/month for Pro (subscription layer) plus usage-based overages once you exceed the included compute (usage layer). The included compute is generous enough that most users never see the usage layer at all, which keeps the perceived pricing simple. But the heaviest users — the ones consuming the most compute — pay proportionally to their consumption. The unit economics stay aligned.

For founders building or repricing a SaaS today, this is the model to plan around. Even if you only have one AI feature now, structure your pricing page so that a usage layer can be added cleanly later. Don't bake "unlimited AI" into your subscription tiers — that's a commitment you'll regret. Read more on the tactical layer of how to add usage-based pricing — it's the tactical companion to this post.

Why outcome-based pricing won't fully replace subscription pricing

A separate narrative is making the rounds on LinkedIn: outcome-based pricing is the future, and within a few years no SaaS company will charge subscriptions anymore — everyone will charge per successful outcome. Pay $1 per resolved support ticket. Pay $5 per booked sales meeting. Pay nothing if the product doesn't deliver.

The pitch is appealing because it sounds aligned: the vendor only wins when the customer wins. Intercom's Finn agent is the canonical example — billed per successful AI-resolved ticket rather than per seat. Some smaller experiments in legal tech and sales tooling are doing similar things.

We don't think this is going to be the new default, and the reason is psychological, not technical.

Customers want predictable budgets. CFOs want predictable budgets. The CFO who approves $50,000/year for Intercom can plan around that number. The CFO whose support tool charges $1 per ticket and the ticket volume swings month-to-month has a much harder time forecasting. When outcome-based pricing produces a higher bill than the equivalent subscription would have, customers feel surprised and resentful — even when the value delivered is objectively higher. Loss aversion beats math, every time.

Intercom's specific case worked because Intercom was already expensive. Customers welcomed outcome-based pricing because it usually meant paying less. That's a one-time arbitrage opportunity for incumbents whose subscription pricing was bloated. It's not a generalizable model.

What's actually going to happen, in our view: subscription pricing will remain the default for the predictable parts of SaaS, usage-based pricing will become a standard add-on layer (covered above), and outcome-based pricing will appear as a niche option for specific high-value AI workflows where the per-outcome value is large enough to justify the variable-cost anxiety. A sales AI that books meetings might charge per booked meeting. A legal-review AI might charge per reviewed contract. But the marketing automation tool that lives next to the sales AI will still charge $99/month.

The teams pivoting to 100% outcome-based pricing because LinkedIn is saying it's the future are taking on a real risk: their cash flow becomes harder to predict, their customer base self-selects toward the kinds of buyers who don't mind variable bills (which is a smaller pool than you'd think), and they lose the ability to confidently project revenue. For most founders, that's not worth the marginal alignment improvement.

PLG and SLG aren't a choice anymore — you need both

A parallel shift is happening in go-to-market motion. Five years ago, the strategic decision was "are we a product-led growth company or a sales-led company?" Bottom-up tools like Slack and Notion ran PLG. Top-down tools like Salesforce and Workday ran SLG. The two models were structurally different and rarely overlapped.

AI is collapsing that distinction. Even pure-SLG enterprise vendors now have to let prospects experience the AI before signing — you can't pitch an AI capability cold over a sales call, because the buyer's first question is "show me." That forces a product-led surface even into enterprise sales cycles: interactive demos, sandbox environments, limited-quota free playgrounds.

The reverse is also true. Pure-PLG products are now hitting more enterprise-grade considerations — HIPAA compliance, data residency, AI-training opt-outs, SOC 2 reports — that prospects increasingly need to discuss before they'll commit at any meaningful tier. That forces a sales surface even into bottom-up motions: solution engineers, security review calls, custom contracts for the bigger buyers.

The result: every SaaS company in 2026 needs both motions. Not as a future plan — as a current operating reality. Less Annoying CRM, which has been pure PLG forever, now offers an interactive demo embedded directly on the marketing site so designers and ops people can play with the actual product before signing up. Kyriba, which is the kind of enterprise-only treasury platform that used to require a five-week sales cycle, now offers concierge pilots specifically because their buyers want to see the AI before signing.

The pricing implication: your pricing page needs to support both motions. A self-serve tier that lets the PLG user transact without talking to a human. An enterprise tier with custom contract pricing for the SLG user. The two coexist on the same page. Trying to be only one or the other is now a self-imposed ceiling.

This intersects with how comparison pages get built, too — once you have both PLG and SLG motions, your competitor comparison page needs to address both audiences: a "what's the trial like" frame for self-serve buyers, and a "how does the contract differ" frame for enterprise buyers. Same page, two reader segments.

Pricing psychology vs pricing math — where to spend your time

A common founder anxiety: how much of pricing is psychological tactics (decoys, charm pricing, anchor tiers) versus structural math (cost-plus-margin, unit economics, ARR targets)? The honest answer is that for SaaS, structural math is the 95% — and psychological tactics are the polish that goes on top once the structure is right.

The reason is that software is fundamentally utilitarian. People don't buy SaaS for fun. They buy it because they have a problem and your product solves it. The buyer's mental model is value received vs price paid. If your tier structure makes the math work for that buyer, they buy. If it doesn't, no amount of $19.99-instead-of-$20 charm pricing will save you.

What we tell founders to actually obsess about:

- One to three plans at the subscription layer (not seven; nobody can compare seven)

- A clear upgrade path between tiers that maps to growing usage or new feature needs

- An enterprise option with "talk to sales" pricing for buyers above a clear threshold

- A trial or freemium experience that's right-sized for your AI cost structure (see the freemium section above)

- A usage layer for the AI compute (see the subscription+usage section above)

That's 95% of what matters. Psychological pricing tricks — anchor tiers, decoy options, charm prices — work on the margin. They don't fix a fundamentally misaligned pricing structure.

The one psychological lever that does matter, and that we think will become more important as AI commoditizes feature parity, is brand taste as a pricing signal. Claude and ChatGPT both charge $20/month for their Pro tiers. Functionally similar, but the users who pick Claude are paying for a different kind of curated experience — more measured, more opinionated, more "Anthropic." Users who pick ChatGPT are paying for the layman's tool — broader, more mass-market, less opinionated. The product is similar; the taste is the differentiator, and that justifies parity pricing without a feature-level explanation.

For SaaS founders building in crowded categories, this is the place to invest creative energy. You won't out-pricing-tactic the competitor. You can absolutely out-taste them — which is the same point we make in Marketing Lessons from Lord of the Rings about Gondor vs Rohan: cultural register is the differentiator once feature parity sets in. Your pricing page is one of the most-visited pages on your marketing site, and it's where the taste signal lands hardest.

What to do this quarter

The transition to Software 3.0 pricing is happening. The teams who are ahead of it are running quiet experiments now. The teams who are behind it will discover the margin compression in their next investor update.

A reasonable starting list:

- Audit your AI cost per active user. If you don't know what each free, trial, and paying user costs you in OpenAI/Anthropic/Google fees, get this number first. Without it, every other decision is guesswork.

- Decide what to do about freemium. Cap it, paywall it, or replace it with a time-limited trial. There's no universally right answer; there's just the wrong answer of pretending the cost structure didn't change.

- Sketch the usage layer. Even if you don't add usage-based pricing this quarter, sketch what it would look like. Credits or tokens? Included in subscription or sold separately? Whose cost does it cover? Run the model. (See the usage-based pricing for SaaS post for the tactical guide.)

- Pressure-test your tier structure against PLG and SLG. Can a self-serve buyer transact without talking to anyone? Can an enterprise buyer find the path to a custom contract? If either is broken, fix it before the next pricing experiment.

- Talk to ten customers about how they think about AI pricing. Their mental models matter more than what LinkedIn experts are saying. Buyers' instincts about variable bills, credit systems, and usage caps will tell you which patterns your specific customer base will tolerate.

The window to get this right is open now. The cost of being wrong compounds with every month of mispriced active users.

Frequently asked questions

"Do I really need a usage layer if I only have one or two AI features?"

Not yet, but the architecture decision matters now even if the implementation comes later. If you bake "unlimited AI usage" into your current subscription tiers, you've made a promise that's hard to walk back when the AI features expand. The fix is to be upfront in your current pricing language: "Pro includes 500 AI actions per month; additional usage available." Even if you never charge for the overages right now, the structural language is in place for when you do. Customers don't get angry when you charge for usage you said you'd charge for from the start; they get angry when "unlimited" turns into "actually, here's a cap."

"How do I know what to price the usage layer at?"

Start with your cost. If a typical AI action costs you $0.05 in OpenAI fees, your credit pricing needs to recover at least that with margin — say, $0.10 per action (50% gross margin) or $0.15 (67% gross margin). The exact margin depends on what other costs you're absorbing (engineering, model fine-tuning, support). Be careful about pricing the layer at cost or below — Cursor subsidized compute heavily to acquire users and is now in the painful position of needing to reprice upward, which always angers existing users. Better to start with a sustainable margin and offer volume discounts later than to start cheap and have to raise prices.

"Will buyers tolerate variable monthly bills?"

Most will, if the variability is bounded. Pure outcome-based pricing — where the entire bill is variable and unpredictable — produces the most anxiety. A subscription + usage layer, where the subscription is fixed and the usage portion is bounded by credits the buyer purchased, produces much less. The framing matters: "you buy $50 in credits when you want them" feels safe; "you're charged a variable amount every month based on what you do" feels scary. Even though they're functionally similar, the buyer's mental model is different. Design the variable layer as a prepaid credit purchase rather than a pay-as-you-go meter when you can.

"How does PLG + SLG reality affect what I show on my pricing page?"

Your pricing page should let both audiences self-route. The self-serve PLG buyer should see clear monthly prices for the Starter and Pro tiers, with a Sign Up button on each. The enterprise SLG buyer should see a clearly-marked Enterprise tier with "Talk to Sales" and a list of what gets added (custom contracts, SLAs, dedicated support, security review). The mistake we see most often: pricing pages that try to be self-serve only, with no enterprise option visible, which forces every large buyer to hunt for the contact form. The opposite mistake: pricing pages where every tier says "Talk to Sales," which kills product-led conversion for the smaller buyers who would have transacted self-serve. Both audiences need to find their path within five seconds of landing on the page.

"Should I be worried about competitors who haven't repriced for AI yet?"

In the short term, no — they're attractive options for buyers because they look cheap. In the medium term, they're going to either (a) eat the margin compression and run out of runway, (b) raise prices abruptly and lose customer trust, or (c) reprice gracefully and end up looking like you. The graceful repricers will be fine; the others will be in trouble. Your job isn't to match their pricing today — it's to build a pricing structure that compounds margin per active user over time. The market will sort the rest out.

"Where does positioning fit into all this?"

Positioning shapes pricing more than most founders realize. If you've done the foundational work to know who you're for, who you're not for, and what specific job your product is hired to do, your pricing tier structure writes itself: Starter is for users at job stage X, Pro is for users at stage Y, Enterprise is for users at stage Z. Without positioning, founders end up trying to make every tier work for every customer — which produces incoherent feature gating and the dreaded "wait, what's actually in Pro?" confusion. This is the deeper version of the three phases of SaaS marketing point: positioning, customer research, and switch analysis are the foundation that makes downstream decisions like pricing tier structure go from agonizing guesswork to obvious choices.